Homebuying Do's and Don'ts

Protect Your Path to Homeownership.

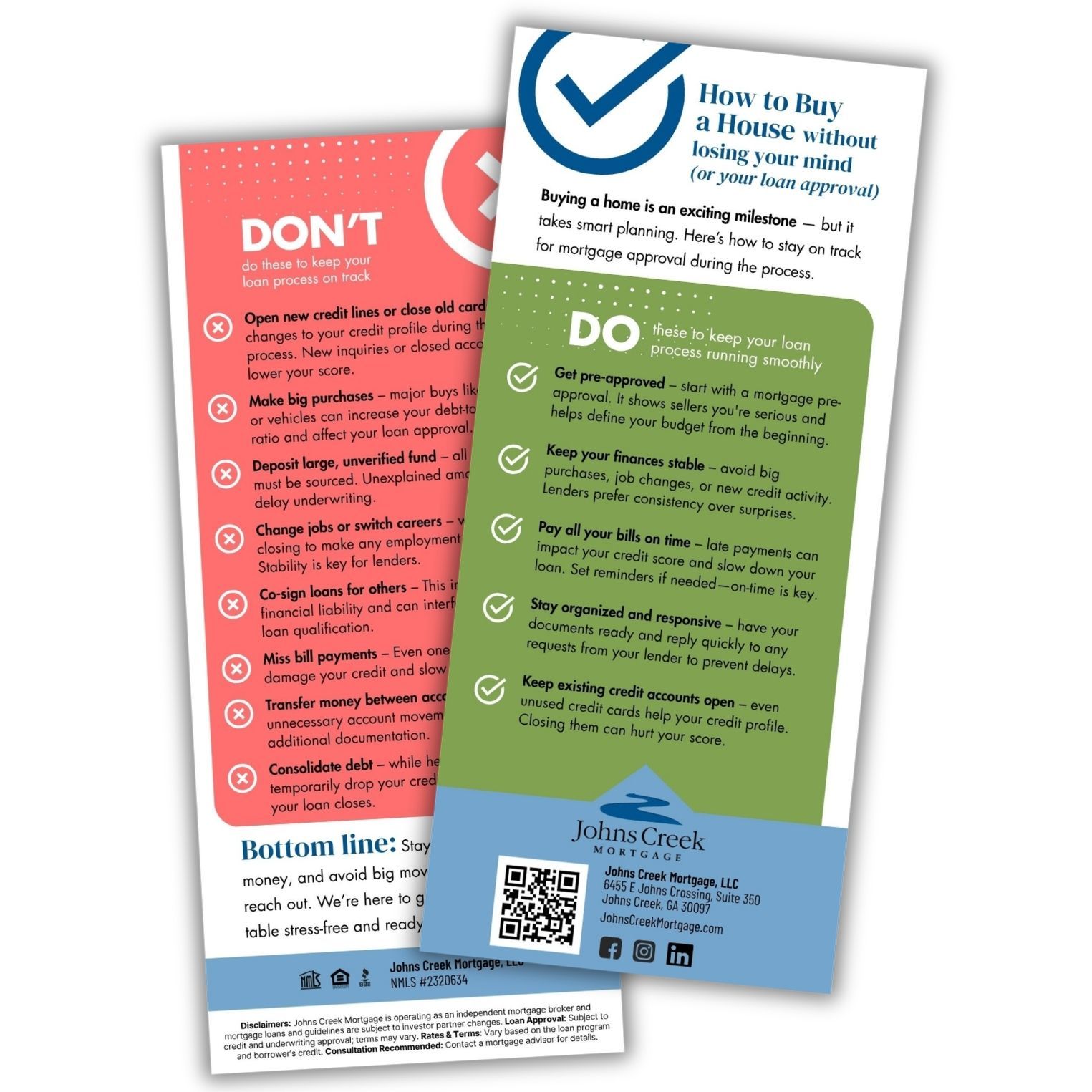

Buying a home is exciting, but it's also important to stay financially consistent throughout the mortgage process. Even small changes to your credit, employment, or finances can affect your loan approval. The good news? A few simple habits can help keep your homebuying journey on track.

At Johns Creek Mortgage, we're committed to providing trusted guidance and clear communication every step of the way. Here's what you should know as you move toward closing day.

Get Pre-Approved Early

A mortgage pre-approval helps you understand your budget, strengthens your offer, and allows you to shop with confidence.

Keep Your Finances Stable

Consistency is important during the mortgage process. Continue managing your finances responsibly and avoid unnecessary changes whenever possible.

Pay Your Bills on Time

Your payment history plays an important role in your credit profile. Staying current on all obligations helps support a smooth mortgage process.

Stay Organized and Responsive

Be prepared to provide documentation when requested and respond promptly to communications from your loan team.

Keep Existing Credit Accounts Open

Even accounts you don't actively use can contribute to your overall credit profile.

Opening New Credit Accounts

New credit inquiries and additional debt can affect your loan qualification and credit profile.

Consolidating Debt During the Loan Process

While debt consolidation may be beneficial in some situations, it's generally best to discuss any major financial changes with your loan consultant first.

Depositing Large Unverified Funds

Lenders are required to verify the source of funds used in a mortgage transaction. Unexpected deposits may require additional documentation.

Changing Jobs or Careers

Employment changes can affect your loan approval. Always consult your loan consultant before making significant career moves.

Co-Signing for Another Loan

Co-signing creates additional financial obligations that may affect your mortgage qualification.

Missing Payments

Even a single late payment can impact your credit profile and delay the mortgage process.

Moving Money Between Accounts

Unnecessary transfers can create additional documentation requirements and slow the underwriting process.

Making Large Purchases

Major purchases such as furniture, appliances or vehicles can impact important qualifying factors during the loan process.

The Bottom Line

The mortgage process works best when your financial picture remains consistent from application to closing.

If you're considering a major financial decision and aren't sure how it could affect your loan, reach out to our team. We're here to answer your questions, provide guidance and help you move forward with confidence.